It’s not always instant, and limits can be tricky. As a financial expert, I’ll break down Chime’s transfer system so your money moves when and where you need it, without the usual fintech headaches. understanding credit card balance transfers can help you save money on interest and consolidate debt more effectively. By taking advantage of introductory offers and lower rates, you can manage your expenses better.

Ever felt like the Pony Express could move your money faster than some neobank transfer delays? You’re not alone! Many Chime users, like Tara (the Gig Worker) who often tells me, “My Chime direct deposit delays impact my bills!”, get caught by unclear digital banking transfer thresholds and confusing Chime transfer times.

This is your expert guide. We’ll cut through the confusion

- About how Chime’s limits really work

- Clarify when your money actually moves

- And I’ll share smart, actionable strategies to transfer faster and more efficiently

I’ll be drawing on my 25+ years of helping clients master the often-tricky fintech money movement rules.

Do You Understand Chime’s Daily Transfer Limits? It’s Not One Size Fits All

Decoding Chime’s Daily Transfer Limits: Why It’s Not One Simple Number

“What’s Chime’s actual daily transfer limit?”

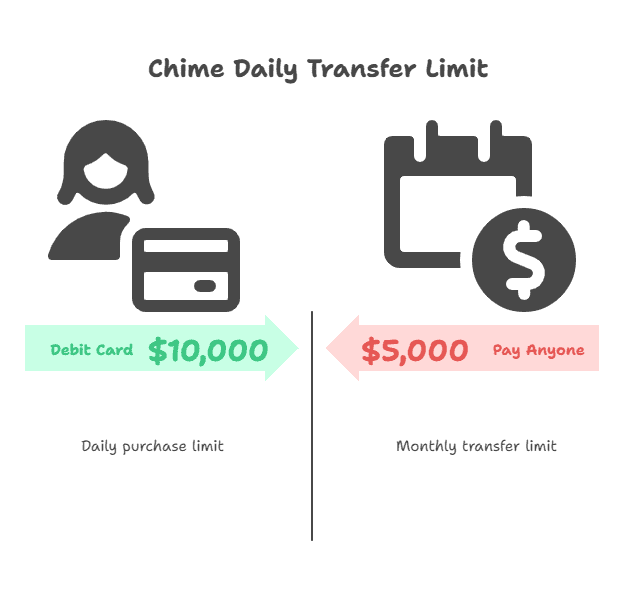

It’s a smart question because Chime’s daily transfer limits aren’t a single figure; they vary dramatically based on how you’re moving money (e.g., ACH, Pay Anyone, debit card purchase) and can even change based on your account’s history, leading to common user confusion.

For instance, your Chime Visa® Debit Card might support purchases up to $10,000 daily, yet using the “Pay Anyone” feature (one of Chime’s instant payout methods) often means a much lower cap of $5,000 per month. This vital difference isn’t always obvious.

I recall David (Small Business Owner) a client who tried to send a $7,000 ACH for a supplier invoice from his Chime account. It bounced. The mistake I helped him fix was understanding this: while Chime can receive larger incoming ACH transfers (some third-party sites like Wise cite up to $10,000/day), sending money out via ACH from the Chime app often hits different, lower internal limits.

These crucial Chime partner banks limits aren’t widely published but are specific to your account, found within your Chime app settings. It’s a critical detail many overlook when dealing with these digital banking transfer thresholds.

Michael Ryan’s Takeaway:

Before any significant transfer, dive into your Chime app (Settings > Account Info > View Limits). This is the ONLY source for your account’s true daily limits for each transfer type, and it’s non-negotiable for avoiding frustrating Chime transfer restrictions.

The Real Speed of Chime ACH Transfers: Beyond the “1-3 Business Days” Window

Tara the Gig Worker often asks, “Why is my Chime transfer taking 3-5 days, sometimes even longer, when I need that cash now?”

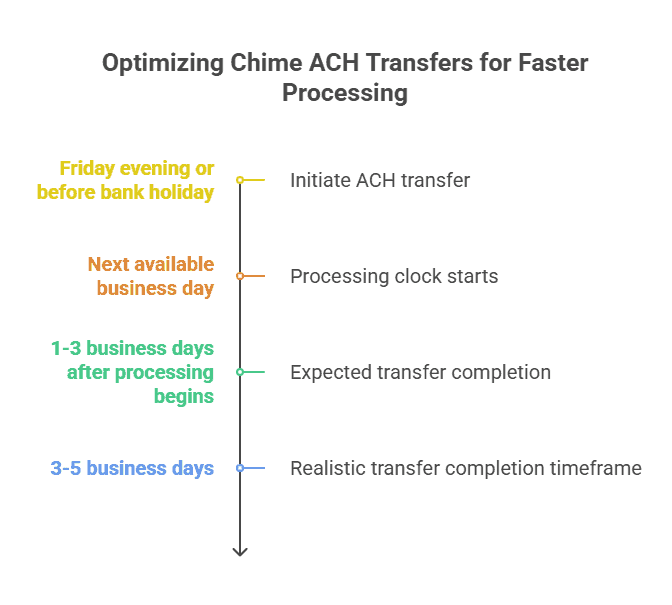

Here’s the reality: while Chime states standard ACH transfers from your account to an external bank typically take 1-3 business days, this often stretches to 5 business days or more. This is due to how Chime’s partner banks (Stride Bank, N.A. or The Bancorp Bank) process these transfers under the fintech money movement rules set by NACHA, which governs the ACH network.

While Chime’s early direct deposit feature is a win for incoming funds, sending money out via ACH follows a slower, more traditional banking rhythm. This is central to understanding Chime ACH vs wire transfer differences (Chime doesn’t typically offer outbound wires for most users).

Is the app’s convenience worth these potential neobank transfer delays? For many, yes, with proper planning.

Need Money Moved NOW? Chime’s Instant Transfer Options (and Their Secrets)

“Does Chime really offer instant transfers, and what’s the catch?”

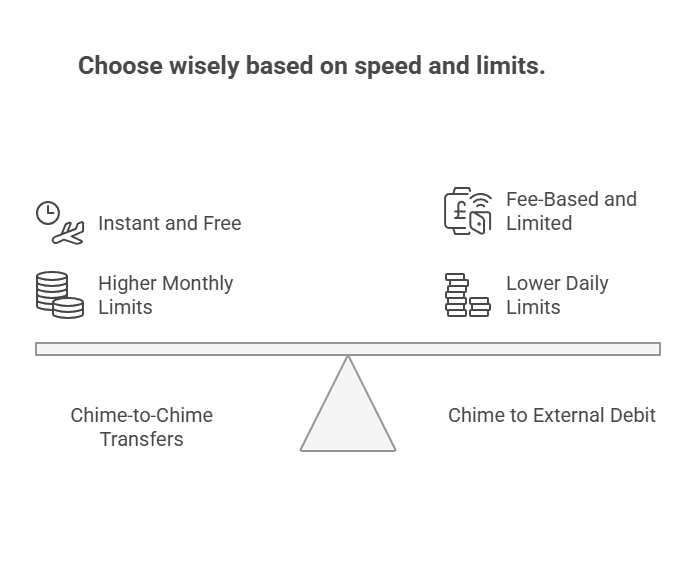

This is a critical question when you need funds moved immediately. Yes, Chime provides faster real-time money transfers than standard ACH, mainly via its “Pay Anyone” feature for Chime-to-Chime transactions and fee-based instant transfers out to an external debit card.

However, both have specific limits and conditions that catch many users, like “Emma the Gig Economy Worker,” by surprise. Are these instant payout methods** always the best choice? Not always.

Tara, another client, easily sent $800 instantly and free to a fellow Chime user via Pay Anyone. But her attempt to instantly transfer $1,200 from Chime to her traditional bank’s debit card for an urgent bill? It failed.

1.75% of the transfer amount as of December 2025

Likewise, instant transfers into Chime from an external debit card often have restrictive monthly caps. While “Pay Anyone” is instant between Chime members and has a higher monthly limit (up to $5,000 as per Chime’s blog), daily caps or Chime transaction velocity limits can still apply. Non-Chime recipients might also wait up to 14 days if they don’t claim funds quickly.

Critical advice: Don’t rely on large instant external transfers for time-sensitive payments without checking your specific Chime app limits first. A Chime Pay Anyone failure often stems from these hidden sub-limits.

Michael Ryan’s Takeaway:

For true instant needs between Chime users, “Pay Anyone” is king. For instant transfers to external debit cards, brace for fees and much lower limits than ACH. Your Chime app reveals your personal limits – check it first!

The Million-Dollar Question: Can You Actually Get Your Chime Transfer Limits Increased?

“Can I somehow get my Chime transfer limits increased?”

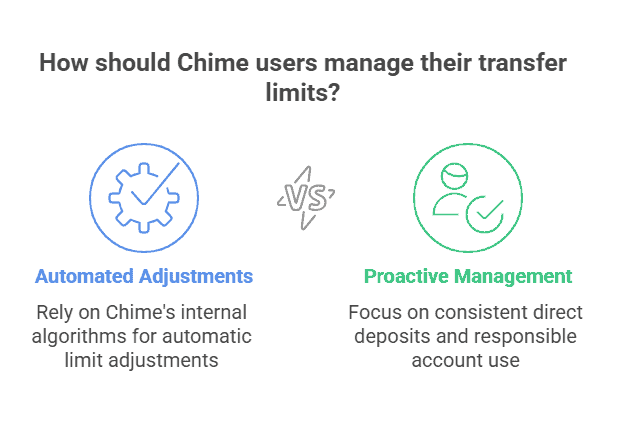

This question, often laced with frustration, lands in my inbox regularly. Generally, Chime’s transfer limits are set dynamically based on your account history, usage patterns, and direct deposit activity. While Chime may adjust limits automatically, there isn’t a formal process for users to request a specific increase for most standard transfer types.

This is a common pain point, especially for users like “David the Small Business Owner,” whose transaction needs can evolve. So, are you completely at the mercy of Chime’s algorithms? Mostly, but there’s a key influencer.

While Chime’s help pages state limits “may change at any time,” this usually means Chime is making system-wide or automated account-specific adjustments based on risk algorithms, not direct user pleas. The common mistake is thinking you can call support to negotiate a higher daily ACH limit for a one-off large payment, as you might with a traditional bank.

With most fintechs like Chime, it’s more automated. However, here’s the crucial part: consistently receiving direct deposits into your Chime account is a significant factor. It can positively influence Chime’s internal reviews, potentially leading to more favorable automatic adjustments to features or certain limits over time, like for SpotMe® or MyPay℠ eligibility.

What not to do:

Assume your limits are unchangeable or that a quick call will magically raise them for a big transfer. Consistent, responsible account behavior, especially with direct deposits, speaks louder than requests.

Michael Ryan’s Takeaway:

While directly requesting higher Chime transfer limits for standard outbound transfers is usually not an option, a healthy account with regular direct deposits is your best lever for potentially seeing positive, automatic limit adjustments over time.

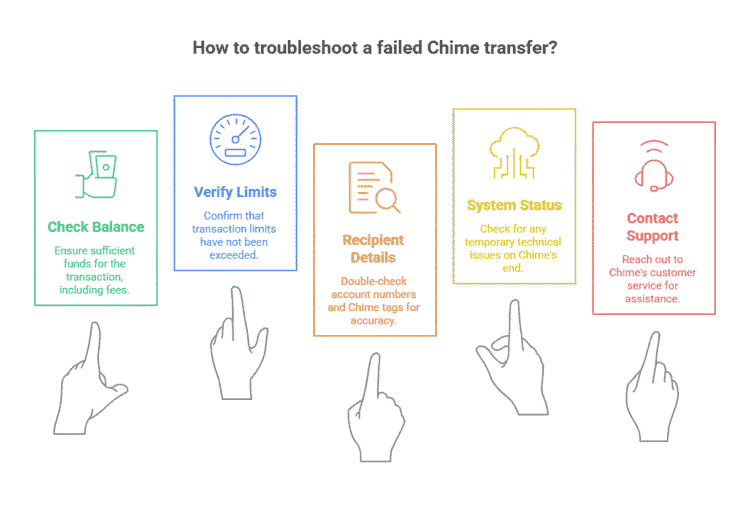

Transfer Turmoil? Why Your Chime Transfer is Pending or Failing (And How to Fix It!)

“Help! My Chime transfer is pending, or it just failed! What do I do now?”

That wave of panic is all too common, especially with important payments looming. Chime transfers can stall or fail for several key reasons: insufficient funds, exceeding your specific transfer limits (daily, per-transaction, or monthly), incorrect recipient details, temporary network hiccups, or security reviews by Chime or their partner banks (Stride Bank, N.A. or The Bancorp Bank).

But what does that mean for you in the heat of the moment?

I worked with “Emma the Gig Economy Worker,” whose Pay Anyone payment to a collaborator kept getting rejected. The mistake she was making (a common one!) was this: while her transfer was under her overall monthly Pay Anyone limit, it was likely tripping a smaller, often unstated per-transaction or daily Chime transaction velocity limit.

Chime’s automated security flags these rapid or unusual patterns. We found that splitting the payment into smaller, separate transfers did the trick.

Another frequent offender? Simply trying to send more than your available balance (don’t forget potential fees!). If an ACH transfer stays “pending” beyond 3-5 business days with no update, it’s absolutely time to investigate. A word of caution: If a large transfer fails, don’t immediately hammer the “send” button multiple times.

This can sometimes trigger more security flags. Pause, take a breath, and troubleshoot methodically.

Here’s your quick Chime transfer troubleshooting checklist:

- Balance Check: Is there truly enough, considering any fees?

- Limit Verification: Dive into your Chime app (

Settings > Account Info > View Limits). Did you hit a daily, per-transaction, or monthly cap? - Recipient Accuracy: Meticulously re-verify account/routing numbers (for ACH) or the recipient’s Chime tag/@ChimeSign (for Pay Anyone). One typo can stop everything.

- Chime System Status: Rarely, Chime might have a blip. Check their official social media or for widespread user outage reports.

- Contact Chime Support: If all else fails, it’s time to contact Chime’s customer service. Use the in-app chat or call (1-844-244-6363 – always confirm this number on Chime’s official site/app). Have all transaction details (dates, amounts, recipient) handy.

Michael Ryan’s Takeaway:

Don’t panic over a pending or failed Chime transfer. Systematically check your balance, your specific limits, and recipient info. If still stuck, Chime support is your next call – be prepared with details.

lance, your specific limits, and the recipient’s details. If the issue persists, promptly contact Chime support with all your transaction information.

Your Top Chime Transfer Questions Answered (FAQ)

Your Top Chime Transfer Questions Answered (FAQ)

- Q1: Why is my Chime ACH transfer delayed?

- A: Chime ACH transfer times can be impacted by initiating after daily processing cutoffs (around 5 PM ET), weekends/bank holidays (they only process on business days), standard NACHA network processing (batching by Chime’s partner banks, Stride Bank or The Bancorp Bank), or occasional security reviews. For these fintech money movement rules, always allow 3-5 business days.

- Q2: Can I speed up a Chime transfer that’s already in progress?

- A: Unfortunately, no. Once an ACH transfer is in the banking network, its speed is fixed by ACH timelines. For future urgent needs, consider Chime’s “Pay Anyone” (Chime-to-Chime) or their fee-based Chime instant transfer to an external debit card, but remember their specific limits for these instant payout methods. Proactive planning beats reactive wishing every time.

- Q3: How do I see my specific Chime transfer limits?

- A: The only reliable source is your Chime app: Go to Settings > Account Info > View Limits. This shows your specific daily/monthly caps for various Chime banking limits. Make this your pre-transfer ritual!

- Q4: What are Chime transaction velocity limits?

- A: Beyond published dollar limits, Chime uses “velocity limits”—undisclosed rules monitoring the frequency and pattern of your transactions. Too many rapid transfers might trigger a temporary hold for security, even if you’re under the dollar cap. This is a standard fraud prevention measure in digital banking transfer thresholds.

- Q5: Do Chime partner banks (Stride Bank, The Bancorp Bank) affect my transfer limits or times?

- A: Yes, indirectly. As the FDIC-insured processors of your Chime transactions, their adherence to NACHA rules and internal schedules directly influences overall timing. Understanding these Chime partner banks limits and processes explains why not all digital transfers achieve true real-time payments (RTP) speed, unlike newer systems such as FedNow.

Michael Ryan’s Action Plan: Take Control of Your Chime Transfers

Navigating Chime transfer limits and Chime transfer times might initially seem daunting, especially with the unique fintech money movement rules at play. However, armed with the right knowledge, it doesn’t have to be a source of ongoing frustration.

While Chime offers exceptional convenience with features like early direct deposit and efficient “Pay Anyone” transactions, mastering your money movement comes down to understanding the distinct operational realities of standard ACH transfers versus real-time money transfers, and crucially, always knowing your account-specific daily and monthly caps.

Remember, your Chime app is your ultimate command center for verifying personal limits.

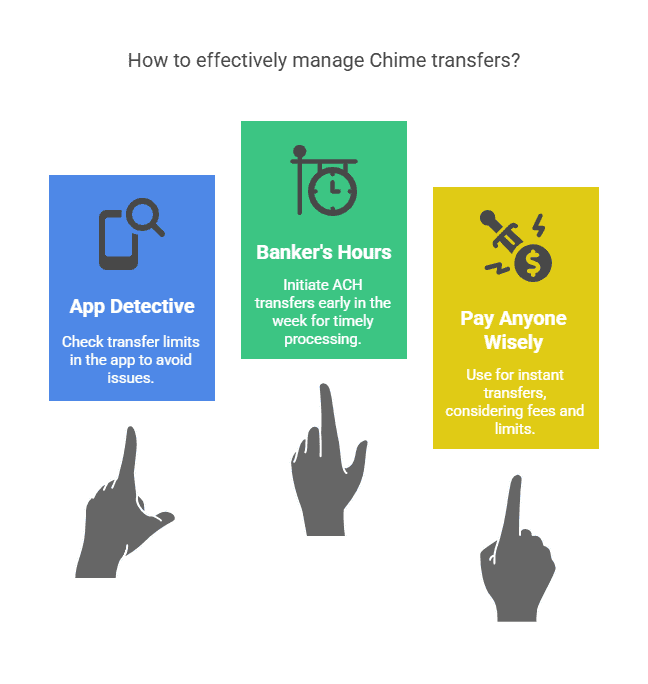

Here are my top 3 action steps to help you master your Chime transfers and steer clear of those frustrating neobank transfer delays:

- ✅ Become an App Detective: Make it a non-negotiable habit. Before any significant transfer, dive into your Chime app:

Settings > Account Info > View Limits. Know your numbers.

This simple check is far more reliable than generic online info and can save you a world of trouble. - 🗓️ Master “Banker’s Hours” for ACH: For non-urgent external bank transfers out of Chime, initiate them early in the week (Monday or Tuesday morning is prime) to maximize the chances of them clearing within that 3-5 business day window.

These are essential ACH timing optimization tips, a stark contrast to hoping for instant results from a system not built for it. - ⚡ Use “Pay Anyone” Strategically: It’s a fantastic tool for instant, fee-free transfers to other Chime users. When considering moving funds instantly to an external debit card, however, be acutely aware of the associated fees and typically much lower limits.

Always ask: is the speed truly worth the cost and constraint for this particular situation, or would a well-planned ACH transfer be smarter?

As the financial world accelerates with digital platforms and innovations like FedNow (explore its objectives on the Federal Reserve’s site), understanding these operational nuts and bolts becomes even more vital.

Apply these insights, and Chime can be a truly powerful and efficient ally in your financial toolkit, ensuring your money moves smoothly, predictably, and precisely when you need it.

What’s your biggest Chime transfer challenge, or what’s one pro tip you’ve discovered for navigating Chime’s limits effectively? Share your wisdom in the comments below – your experience could be the key to helping someone else!

💡 Want more fintech money tips like these, straight from a seasoned financial planner? Get my printable Chime Transfer Limit Cheat Sheet (PDF) when you subscribe to my newsletter!

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.