Converting hourly wages to annual salary isn’t complicated—it’s basic division. But the federal minimum wage hasn’t budged from $7.25 since 2009, while 18 states are raising their minimum wages in 2026, some to $16+ per hour. That means your hourly rate matters more than ever for negotiating pay, budgeting, and comparing job offers.

Whether you’re negotiating a job offer, budgeting for expenses, or simply trying to grasp your earnings, understanding this figure is crucial.

Quick Calculation Tip: To convert an annual salary to an hourly wage, simply divide your annual salary by the total hours you work in a year. For most full-time jobs, that’s about 2,080 hours (40 hours a week times 52 weeks).

Step-by-Step: How to Calculate Your Hourly Wage from Annual Salary

Annual Salary to Hourly Wage Calculator

To help you calculate your hourly wage, consider using an annual salary to hourly wage calculator. Here’s a simple example of how the calculator can work:

[hourly_wage_to_annual_salary]

Basic Formula

To find your hourly wage, use the formula:

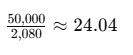

Formula: Hourly Wage = Annual Salary / Total Working Hours per Year

For a standard full-time employee working 40 hours a week for 52 weeks, this means:

Total Working Hours per Year: 40 hours / week × 52 weeks / year = 2,080 hours

Example:

Taxes and Benefits: Your gross pay doesn’t reflect what you take home. Deductions for income taxes, health insurance, and retirement contributions can significantly reduce your net pay.

- To estimate your net hourly wage, calculate your effective tax rate and subtract it from your gross pay. Also, account for any regular deductions for benefits.

- Variable Hours: If your work schedule varies, adjusting your calculations based on actual hours worked per week and weeks worked per year is essential.

Conclusion

The math is straightforward—divide your annual salary by 2,080 hours to get your hourly rate. But context matters: with the federal minimum wage frozen at $7.25 since 2009 and average hourly earnings hitting $31.46 in August 2025, knowing your exact hourly wage helps you evaluate job offers and negotiate raises based on real market data, not guesswork.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.