Have a High Deductible Health Plan (HDHP)? Maybe you chose it for the lower premiums, but now you’re wondering how best to manage those higher potential out-of-pocket costs. What if I told you the key to managing those costs is a tax-advantaged medical savings account that can double as a stealth retirement vehicle?

According to the Employee Benefit Research Institute (EBRI), HSA assets have surged significantly, showing their growing popularity among savvy savers.

It’s a common situation; navigating healthcare expenses can feel like a constant balancing act. But what if the account designed for today’s health expenses was actually one of the most powerful retirement savings tools available, hiding in plain sight?

There’s a critical factor many people miss about Health Savings Accounts (HSAs) – they are far more than just a way to pay doctor bills. In the next few minutes, I’m going to show you exactly why the HSA might be the most valuable financial account you didn’t know you needed, and how you can leverage its unique power.

What Exactly IS a Health Savings Account (HSA)? The Basics

Alright, let’s break it down simply. Think of a Health Savings Account, or HSA, like your own personal savings vault specifically for healthcare expenses. It’s an account you own – not your employer, not the insurance company.

You can watch this quick slideshow to get a better understanding of how you can take advantage of the HSA. Just press play, then continue reading.

To open and contribute to one, you generally need to be enrolled in a specific type of health insurance called a High Deductible Health Plan (HDHP), which we’ll cover next.

The money you put into this “vault” can be used for qualified medical costs (IRS Pub 969) anytime, now or in the future. Unlike some other accounts, the money is yours to keep and rolls over year after year. There’s no “use it or lose it” pressure. But here’s where it gets really special.

The HSA has what many call an unbeatable Triple Tax Advantage. We’ll dive deep into this soon, but conceptually, it means potential tax breaks when you put money in, when it grows, and when you take it out for medical needs. It’s a unique combination that makes this health vault incredibly powerful.

Are You Eligible? The HDHP Connection is Key

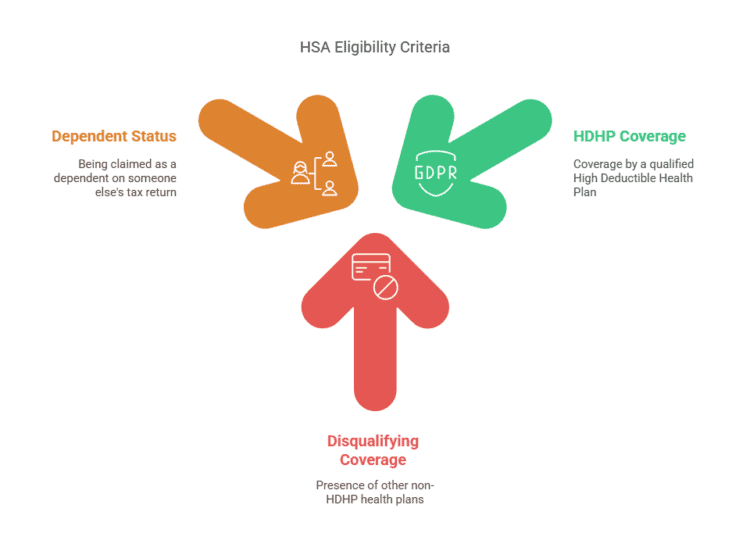

Eligibility for an HSA isn’t automatic; it hinges primarily on your health insurance. Let’s run through the checklist precisely, referencing the official rules from the Internal Revenue Service (IRS):

- ✅ Are you covered by a qualified High Deductible Health Plan (HDHP)?

This is the main gatekeeper. An HDHP has a higher deductible than traditional plans but often lower monthly premiums. - For 2025, the IRS defines an HDHP as having a minimum annual deductible of $1,650 for self-only coverage and $3,300 for family coverage. There’s also a maximum out-of-pocket limit: $8,050 for self-only and $16,100 for family coverage in 2025 (Source: IRS).

- Why the HDHP link? The idea is that you use the HSA funds to cover costs below your high deductible, empowering you to manage your own health spending with tax advantages. You can find consumer-friendly explanations at Healthcare.gov.

- ✅ Do you have other disqualifying health coverage?

You generally cannot contribute to an HSA if you are also covered by another non-HDHP health plan (like a spouse’s traditional plan), Medicare (Part A or B), or TRICARE.

An exception exists for certain “permitted coverage” like dental, vision, or specific disease policies. - ✅ Can you be claimed as a dependent on someone else’s tax return?

If someone else can claim you as a dependent, you cannot contribute to your own HSA, regardless of your health plan.

Carefully verifying these points, especially your HDHP’s specific deductible and out-of-pocket limits against the current year’s IRS guidelines (found in IRS Publication 969), is crucial.

Contribution Magic: How Much & How It Works

Okay, so you’re eligible – fantastic!

Now, how much can you put into this powerful account, and what are the practical ways to do it?

First, the limits. The IRS sets annual contribution limits. For 2025:

- Self-only HDHP coverage: You can contribute up to $4,300 (up from $4,150 in 2024).

- Family HDHP coverage: You can contribute up to $8,550 (up from $8,300 in 2024).

- Catch-Up Contribution: If you are age 55 or older by the end of the year, you can contribute an additional $1,000 “catch-up” contribution.

Now, let’s talk tactics for getting the money into an HSA:

- Tactic 1: Payroll Deduction (Often the best!): Many employers allow you to contribute directly from your paycheck before taxes. The huge advantage here? These contributions typically avoid both income tax and FICA taxes (Social Security and Medicare), giving you an extra layer of savings!

- Tactic 2: Direct Contribution: You can also contribute directly to your HSA with post-tax dollars and then claim a tax deduction when you file your return.

Important Note for Married Couples:

HSA contribution strategies can get complex. If both spouses have family HDHP coverage, they’re limited to a single family contribution limit ($8,550 for 2025) split between their respective HSAs however they choose.

However, the $1,000 catch-up contribution is per person; if both spouses are 55+, each can contribute an additional $1,000 to their own HSA (subject to the overall family limit structure).

Important Deadline: You generally have until the tax filing deadline (usually April 15th) of the following year to make contributions for the current tax year. So, you have until April 15th, 2026 to contribute for 2025.

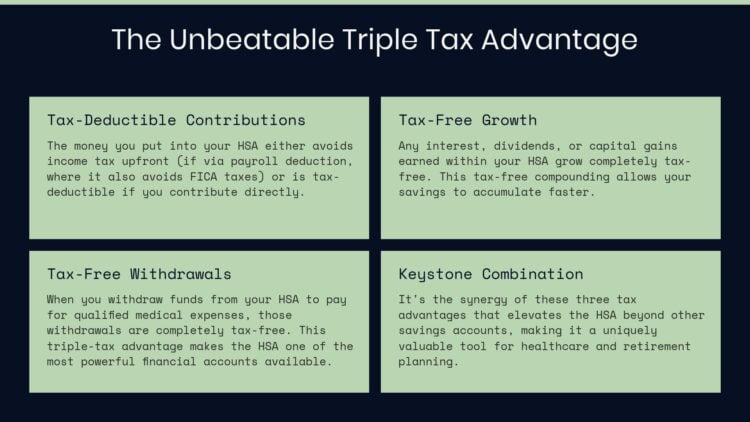

The Unbeatable Triple Tax Advantage of an HSA Explained

We’ve mentioned the “Triple Tax Advantage” – let’s deconstruct precisely why this combination is so uniquely powerful. It’s this combination, this synergy, that elevates the HSA beyond any other savings account.

- Tax-Deductible (or Pre-Tax) Contributions: The money you put in either avoids income tax upfront (if via payroll deduction, where it also avoids FICA taxes) or is tax-deductible if you contribute directly.

- Tax-Free Growth: Your contributions can be invested, and any interest, dividends, or capital gains earned within the HSA grow completely TAX-FREE.

- Tax-Free Withdrawals (for Qualified Medical Expenses): When you withdraw funds to pay for qualified medical expenses – anytime – those withdrawals are completely TAX-FREE.

It’s this Keystone Combination that makes the HSA arguably the most tax-efficient account available in the American financial system. This power is reflected in growing usage: as of mid-2024, total HSA assets surged to $137 billion across nearly 38 million accounts (Source: Devenir Research, Sept 2024).

Account holders using the investment features maintain significantly higher average balances ($20,677), showcasing the impact of tax-free growth (Source: Devenir Research). For a deeper dive into other tax-advantaged options, check out our guide on Roth IRAs vs 401(k)s.

Important State Tax Note:

While these three advantages apply at the federal level nationwide, it’s important to note that state tax treatment can vary. For example, California and New Jersey currently do not recognize HSA tax deductions or tax-free growth at the state level. Remember that state tax treatment of HSAs varies, so check your state’s specific rules when calculating your total tax benefits.

Spending vs. Saving: Qualified Expenses & Long-Term Strategy

Naturally, you can use your HSA funds for a wide range of “qualified medical expenses“. This includes obvious costs like doctor visit co-pays, prescriptions, dental exams, and eyeglasses, but also extends to things like acupuncture, chiropractic care, mental health therapy, smoking cessation programs, certain over-the-counter medications (with prescription sometimes required), and even durable medical equipment like crutches or blood sugar monitors.

The definitive list is maintained by the IRS in Publication 502, Medical and Dental Expenses – it’s worth reviewing.

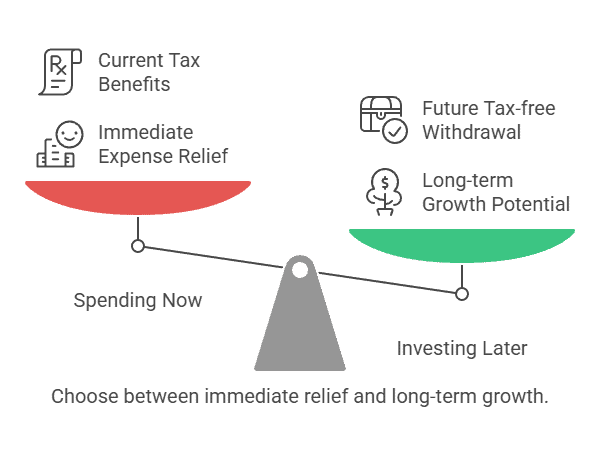

But here’s where we need to reframe the HSA.

Many see it simply as a way to spend pre-tax dollars on current health needs. That’s fine, but it misses the bigger picture.

What if you reframed the HSA not as a spending account, but as a long-term investment vehicle with amazing tax benefits?

Consider this “Secret Sauce” Strategy:

If you can afford to pay for your current qualified medical expenses out-of-pocket with other funds, do it! Then, meticulously save the receipts (scan them digitally!). Why? Because there’s no time limit on reimbursing yourself from your HSA.

Imagine this:

You pay $500 in out-of-pocket medical costs today. You save the receipt. Your $500 stays in the HSA, invested, growing tax-free for decades. Years later, that original $500 might have grown significantly.

Then, you can pull out that original $500 (based on the receipt) completely tax-free. You essentially converted today’s medical expense into a long-term, tax-free investment return.

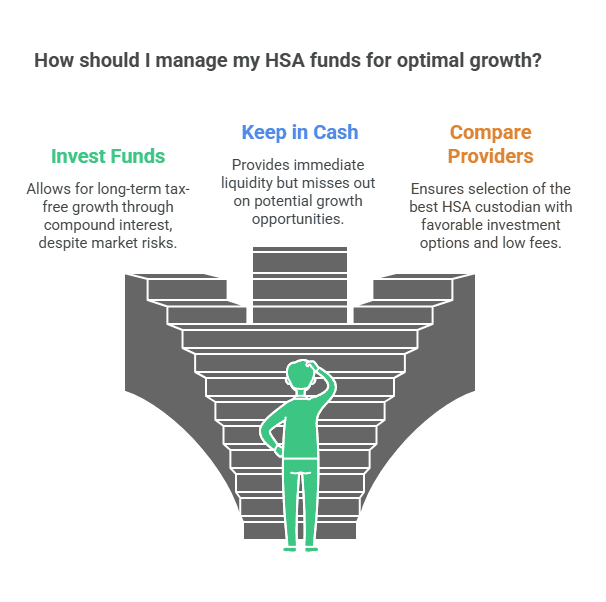

Beyond Savings: Investing Your HSA Funds

Unlike FSAs, most HSA providers allow you to invest your funds once your balance reaches a certain threshold (often $1,000-$2,000). This unlocks the true long-term growth potential through compound interest.

- How it Works: Typically, you’ll transfer funds from the cash portion of your HSA to a linked investment account and choose from options like low-cost index mutual funds or ETFs.

- Risk vs. Reward: Investing involves market risk, but the potential reward of long-term tax-free growth is substantial. Despite HSA investment assets growing significantly (up 21% in the first half of 2024 to $56 billion), only about 9% of accounts have invested portions of their HSA dollars, indicating a huge missed opportunity for many (Source: Devenir Research, Sept 2024).

- Choosing a Provider: When selecting an HSA custodian (or evaluating your employer’s), compare options based on:

- Investment Options: Range and quality, especially low-cost index funds.

- Fees: Administrative, investment, transfer fees. Low fees are crucial.

- Platform Usability: Investing your HSA transforms it into a powerful engine for wealth accumulation.

HSA vs. FSA: Decoding the Alphabet Soup

Let’s clear up the confusion between HSAs and Flexible Spending Accounts (FSAs). Key differences make them distinct:

| Feature | Health Savings Account (HSA) | Flexible Spending Account (FSA) |

|---|---|---|

| Eligibility | Must have HDHP | Offered with various plan types |

| Ownership | You own the account | Owned by your Employer |

| Portability | Yes, stays with you if you change jobs | No, generally forfeit if you leave job |

| Rollover | Yes, funds roll over indefinitely | No, typically “Use-it-or-lose-it” |

| Investing | Yes, usually possible | No |

| Max Limit (’25) | $4,300 (Self) / $8,550 (Family) | Limit set by IRS annually (Lower than HSA) |

Key takeaways: HSAs offer ownership, portability, rollover, and investing – making them superior for long-term savings if you’re eligible.

The HSA in Retirement: Your Secret Health & Wealth Tool

Here’s where the long-term planning perspective truly shines. The HSA transforms beautifully in retirement.

- The Age 65+ Rule Change:

Once you turn 65, you can still withdraw funds completely tax-free for qualified medical expenses (including Medicare premiums for Parts B, D, and Advantage plans!).

Crucially, you can also withdraw funds for any other reason without penalty (though non-medical withdrawals are subject to ordinary income tax, like a Traditional IRA). - The Retirement Power:

This flexibility makes the HSA incredibly potent. According to Fidelity’s research, a 65-year-old couple may need hundreds of thousands ($315k estimated in 2023) just for healthcare expenses in retirement, making a tax-free HSA fund an essential component of a comprehensive retirement strategy.

It’s like having a Traditional IRA plus a dedicated, tax-free medical fund.

HSAs and Medicare: Important Considerations

Understanding how HSAs interact with Medicare is critical as you approach age 65. Here are the key points:

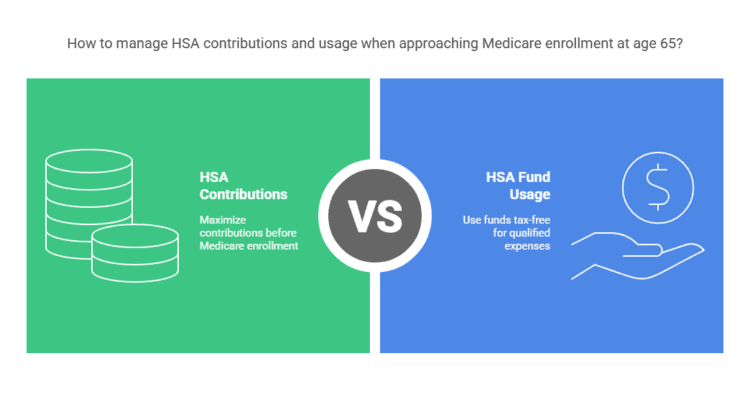

- Contribution Stop:

Once you enroll in any part of Medicare (including Part A, which can be automatic for some receiving Social Security), you can no longer contribute to an HSA. You can pro-rate your contribution for the year you enroll based on the months before Medicare coverage began. - Using Funds:

You can continue to use your existing HSA funds tax-free for qualified medical expenses indefinitely, even while enrolled in Medicare. This includes paying for Medicare premiums (excluding Medigap), deductibles, copays, and other healthcare costs. - Strategic Planning:

If nearing 65, consider maximizing HSA contributions before Medicare enrollment begins. Delaying Social Security might allow you to delay automatic Part A enrollment and continue HSA contributions longer, but consult official Medicare resources and potentially a financial advisor about your specific situation.

Common HSA Mistakes & Myths Debunked

Let’s tackle some common pitfalls:

- Myth #1: “HSAs are ‘Use-It-or-Lose-It’ like FSAs.”

- The Fix: Wrong! HSA funds NEVER expire and roll over indefinitely.

- Mistake #1: Not Contributing (or Under-Contributing).

- Reality Check: Despite tax advantages, the average HSA contribution is often significantly less than the statutory maximum (Source: EBRI, March 2024).

- The Fix: Start small if needed, prioritize employer match, use payroll deduction.

- Mistake #2: Failing to Invest the Funds.

- Reality Check: Only about 13% of accountholders invest their HSA funds (Source: EBRI), missing major growth potential.

- The Fix: Choose a provider with good low-cost options, start investing early.

- Mistake #3: Poor Record-Keeping for Reimbursements.

- The Fix: Scan receipts digitally immediately; use a dedicated folder. Essential for the long-term reimbursement strategy.

Your Next Steps – Taking Advantage of Your HSA To Save For Retirement

So, remember that health account tied to your HDHP? We’ve seen it’s far more than just a way to pay bills. It’s potentially the most powerful triple-tax-advantaged savings and investment vehicle available – a true stealth retirement tool. The key lies in understanding its unique rules and leveraging its long-term potential.

You now have the understanding to move beyond simply having an HSA to truly utilizing it effectively. Check your HDHP eligibility, explore your contribution options (aim for the max!), and consider the long-term investment strategy.

Consider exploring how an HSA fits into your overall financial planning process and complements your other retirement accounts like Roth IRAs. Taking just that one small step—perhaps setting up a small payroll contribution today—puts you back in control and starts building momentum toward both healthcare security and retirement readiness.

When choosing where to open or invest your HSA, compare options from major HSA custodians like Fidelity, Lively, HealthEquity, and others, focusing on fees and investment choices.

Want to truly maximize this account? Understanding how to choose the right investments is crucial. To deepen your understanding, dive into our guide: Smart Investing Strategies for Your HSA Funds.

Take this insight and apply it. You’ve got this!

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.